Coffee prices fell due to high exports and increasing inventory levels

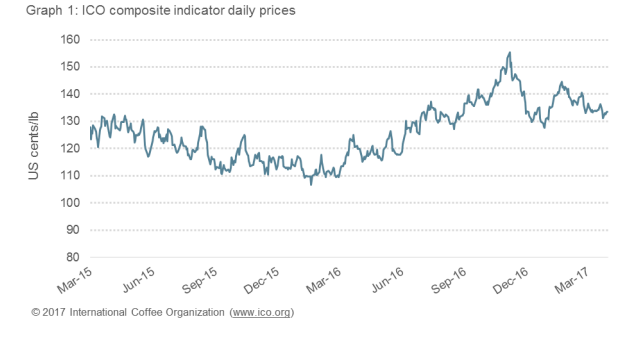

In March, the ICO composite indicator price fell slightly. While Robustas remained broadly stable, Arabica prices were under pressure. Despite the poor Conilon/Robusta harvest in Brazil and Vietnam, the market remained well supplied as export levels in the period October 2016 to February 2017 were higher than the year before, while inventories in importing countries continued to grow.In combination with an increasingly positive outlook for the 2017/18 crop, the market currently lacks any strong signals to reverse from its current gradual decline.

Lastly, it should be noted that at its 119th Session held from 13 to 17 March 2017, the

International Coffee Council appointed Mr José Dauster Sette of Brazil to the post of Executive Director of the ICO for a five‐year term from 1 May 2017.

In March, the ICO composite indicator price continued the slow decline observed since the beginning of the year. The monthly average of the composite indicator was down by 2.6% to 134.07 US cents/lb in March from 137.68 US cents/lb recorded in February.

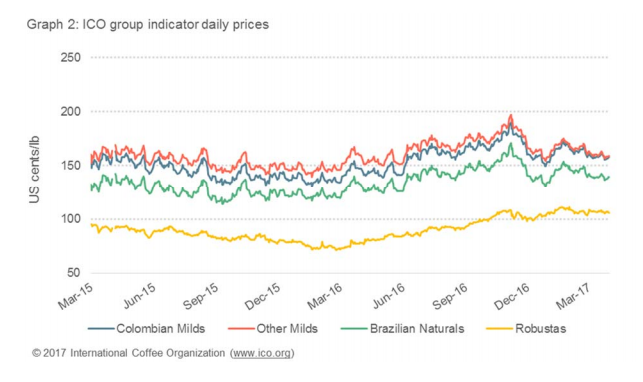

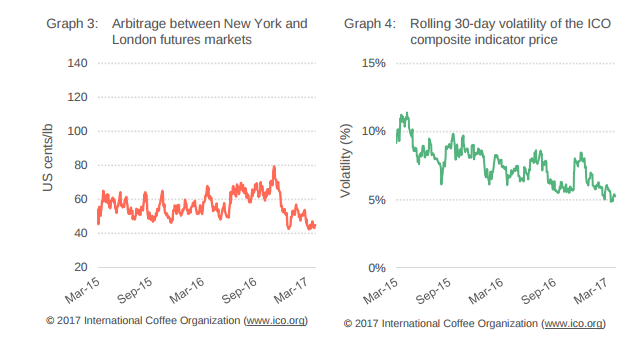

The group indicators were showing a mixed picture. On the one hand, the monthly averages of the Arabica groups significantly decreased, with Colombian Milds, Other Milds and Brazilian Naturals down by 3.2%, 3.7% and 4%, respectively. Prices for Robustas on the other hand remained broadly stable with little in‐month variation. The March monthly average of 106.73 US cents/lb constitutes a marginal increase of 0.2% compared to 106.49 US cents/lb recorded in February. The arbitrage between the London and New York futures markets continued to decrease, down by 11.6% from 50.18 US cents/lb to 44.37 US cents/lb.

The development of coffee prices in March was mainly driven by the fact that supply remained ample despite the poor Conilon/Robusta harvest in Brazil and Vietnam. World market prices for Robusta have been relatively high as indicated by the ICO Robusta indicator price which has been consistently above 100 US cents/lb since October 2016. This has led to the draw down of stocks in Vietnam somewhat compensating for hampered Robusta exports from Brazil. In the first five months of coffee year 2016/17 (October 2016 to February 2017) Vietnam is estimated to have shipped 10.18 million bags, an increase of 11.5% compared to the same period last year.

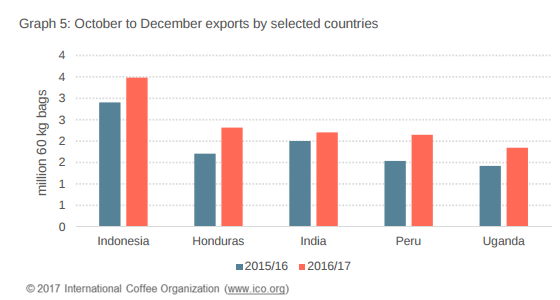

At the same time, Arabica availability on the market remains high. Colombia’s production and exports continue to grow as resistant coffee trees planted following the coffee leaf rust crisis in 2010 have become fully productive. Other producers such as Indonesia, Honduras, India, Peru, and Uganda, which make up almost a quarter of global exports, significantly increased their shipments in the first months of coffee year 2016/17. The highest increase was observed in Honduras with exports totalling 2.31 million bags, up by 35.6% compared to 1.71 million in 2015/16. However, it remains to be seen if this growth is sustainable as reports emerge of a new outbreak of leaf rust in Honduras.

Certified stocks on the New York and London futures markets have increased further by 2.4% (from 1.49 million bags in February to 1.53 million bags in March) and 1.9% (from 2.80 million bags in February to 2.85 million bags in March) respectively. At the same time, inventories in consuming countries continued to build up. For example, in February coffee stocks in the United States reached 6.45 million bags, the highest level since May 2003. In combination with a positive outlook for the 2017/18 crop in Brazil and Vietnam previous supply concerns seem to have been largely alleviated and the market lacks any strong signals to reverse from its gradual decline.

Source: http://www.ico.org/